💰 Refinance or Hold for Now?

How to Make an Informed Decision When There's So Much Noise

If you own a home and you’ve financed it with a mortgage rather than paying cash, there’s a good chance your phone’s been buzzing lately. And, because a lot of those calls are coming from your mortgage holder, you’re more likely to answer them than the usual sales call. But how do you know if all those calls, postcards promising “once-in-a-decade savings,” and maybe even a few emails urging you to refinance before rates rise again are really worth listening to?

It’s tempting to jump on a refinance offer. After all, the Federal Reserve just cut interest rates, and mortgage chatter is everywhere. But the decision to refinance—or hold for now—isn’t one-size-fits-all. Especially not here in the Lakes Region, where seasonal rhythms and property types are as varied as our shorelines.

Let’s break it down.

Why You’re Hearing from Everyone Right Now

Whenever the Fed cuts rates, national mortgage lenders leap into action. Remember though, that while they may make it seem like they’re looking out for you, they have quite a bit to gain from your decision to refinance. After all, their job is to generate new business, so even a modest cut gets the phones ringing.

Refinancing can look straightforward: swap your old mortgage for a new one at a lower rate, lower your monthly payment, and save money. But beneath the surface, a refinance comes with a cluster of hidden or easily overlooked costs, many of which go to the lender that can erode those savings if you’re not careful.

Let’s unpack the most common ones:

Loan Origination and Underwriting Fees are lender-imposed administrative charges for processing your new loan that typically range 0.5%-1% of the loan amount. So on a $400,000 mortgage, a half-point fee would be $2000. You can negotiate these fees — but many borrowers forget to ask.

Appraisal Fees are usually about $500- $1000 in the Lakes Region and are used to determine current market value. See below for more thoughts on how timing matters when appraising.

Title Search, Insurance, & Recording Fees are required even if you’ve only owned the home for a year, cost about $1000-$2500 combined and Lenders may require new lender’s title insurance even if you’re refinancing with the same company.

Escrow Adjustments aren’t a long term cost as your original escrow will be refunded - eventually, but you will have to prepay months of taxes and insurance at the closing for the refinance.

The Local Reality Check

Here in Carroll and Belknap counties, our market doesn’t move in lockstep with the national one. We’ve got everything from classic in-town Capes to lakefront estates and part-time getaways — and that mix makes refinancing here a little less straightforward.

A few quick snapshots paint the picture:

According to NAR data, about 74% of recent buyers nationally financed their home purchases (i.e. 26% of sales were in cash). But, we know that a higher percentage of investors and second-home buyers pay cash, so you can assume that fewer of your neighbors are weighing their options than in most areas of the country.

Over 90% of new mortgages in New Hampshire are 30-year fixed loans — the steady, predictable kind most homeowners prefer.

In Belknap County, roughly 78.7% of homes are owner-occupied.

In Carroll County, that number is closer to 81%. But unlike more urban markets, a large share of those are second homes or seasonal properties, where rates and underwriting rules differ from primary residences.

That means the postcard in your mailbox promising “easy savings” might not tell the full story.

Appraisals can swing widely depending on whether your home is lakefront, lake-access, or tucked in the woods.

And if you’re already holding a rate under 5%, the cost of refinancing — especially once you factor in closing fees — may outweigh the savings for now.

The Crucial Math: Interest Savings vs. Closing Costs

So now that you know that those one-size-fits-all offers may not fit your needs, do the math! One of the most common mistakes is ignoring closing costs when evaluating a refinance.

Estimate your upfront costs.

Appraisal, underwriting, title, and recording fees can easily total 1%–3% of your loan balance. See above for details on why these numbers incentivize lenders to reach out as soon as there’s a rate cut.Calculate your break-even point.

Before you say yes to a refinance offer, add up all the direct and indirect costs.

Then calculate your break-even point:Total Closing Costs ÷ Monthly Savings = Months to Break Even.

If the break-even period is longer than you plan to stay in the home (or longer than your comfort zone), it may be better to hold for now — especially if further rate cuts are possible. Example: If you’ll save $150 per month and pay $4,000 in closing costs, your break-even is around 27 months. If you plan to sell, move, or refinance again before then, the math probably doesn’t work.

And if you’re not sure how to read that “Loan Estimate” your lender sent, Andrea and I are happy to walk you through it. Sometimes a second pair of eyes makes all the difference — especially when the fine print could add up to thousands.

Watch your amortization clock.

Resetting a 30-year mortgage can mean paying more interest over time, even with a lower rate. Even if your rate drops, stretching your remaining 23 years back to 30 can add tens of thousands in lifetime interest.

Example: A $350,000 loan at 5% with 23 years left refinanced at 4% for 30 years saves ~$200/month — but adds ~$25,000 in total interest paid.Ask about lender credits or roll-in options.

Some lenders let you fold costs into the loan—but that increases your principal and long-term cost, so do the math carefully.

If you have a government-backed loan, you might qualify for an easier path. FHA, VA, & USDA Streamlines often offer a refinance option with no income verification or new appraisal required - making it simpler - and cheaper - to refinance.

Timing and the Lakes Region Factor

Refinancing isn’t just about rates. It’s about timing.

In the Lakes Region, winter appraisals can be tricky: driveways unplowed, docks pulled in, seasonal homes half-buttoned-up. Many local lenders recommend waiting until spring, when comparable sales data is stronger and homes show better.

If you’re thinking about a refinance, fall is a perfect time to gather your paperwork, request quotes, and get your ducks (and docks) in a row—without rushing into the first flashy offer that lands in your mailbox.

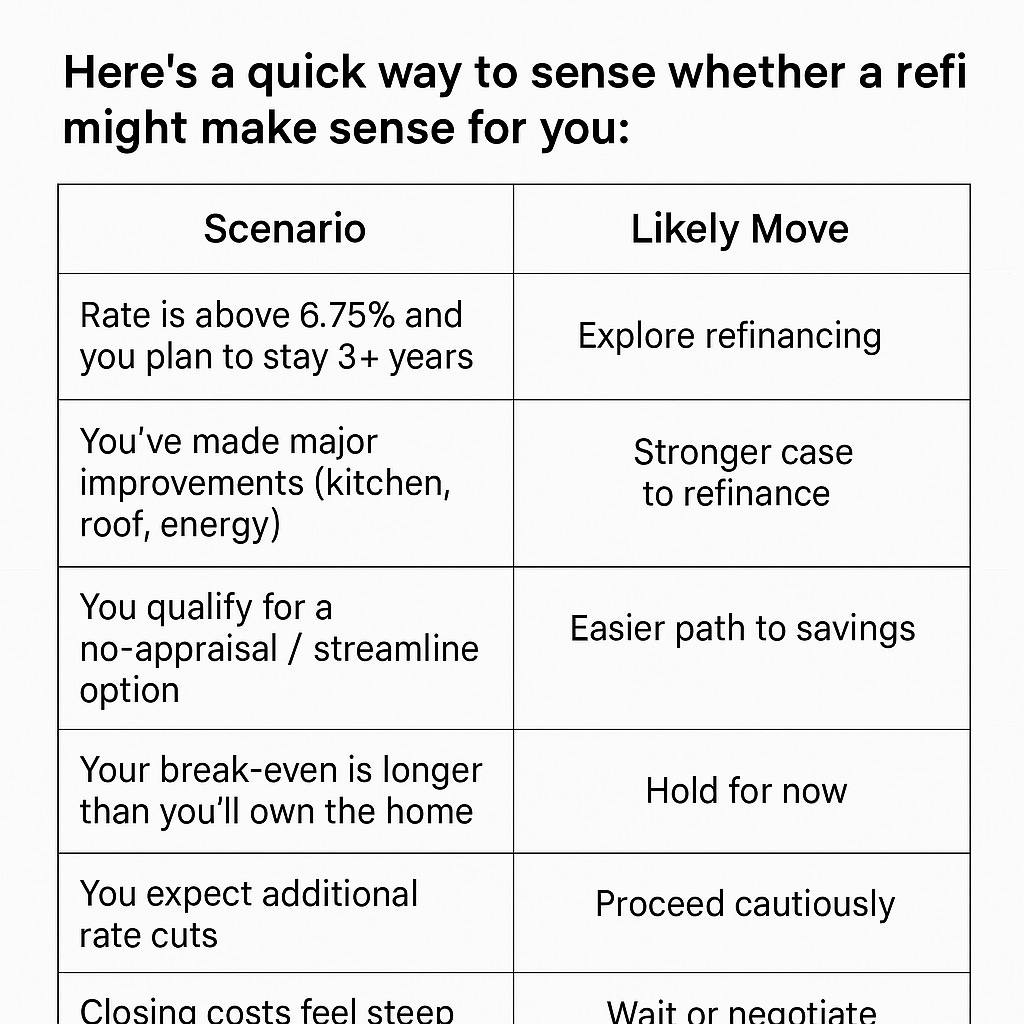

A Few Smart Filters Before You Act

Here’s a quick way to decide whether a refi might make sense for you:

The Bottom Line

Don’t let the marketing noise make your decision for you. The Fed’s move is significant, but its true impact will unfold over the coming months.

The smartest play for many homeowners right now may be to hold for now—keep an eye on local lender rates, calculate your break-even, and reassess when the numbers work clearly in your favor.

If you’d like a no-pressure way to look at your specific numbers—or just want a recommendation for a lender who actually understands the Lakes Region market—Andrea and I are happy to connect you with someone we trust.

Until then, take every “act now” postcard with a grain of salt, enjoy these crisp October mornings, and remember: patience often pays off — for both mortgages and leaf season.